On 14 June 2025, the National Assembly promulgated Law No. 67/2025/QH15 on Corporate Income Tax (CIT Law), which supersedes the consolidated Law on Corporate Income Tax 2008. With its effective date of 1 October 2025 – less than a month away from now – and retroactive application to the entire 2025 tax year, this new legal framework demands prompt attention from all enterprises operating in Vietnam.

Concurrently, to provide detailed guidance for provisions of the new CIT Law, a corresponding draft guiding Decree (Draft Decree) has been released by the Ministry of Finance (MOF) for public comment, and is well expected to be finalised and issued prior to the CIT Law’s effective date.

Below are key takeaways of the CIT Law and the Draft Decree for your reference.

Expanded definitions of taxpayers and permanent establishments

To manage tax efficiently in the era of digital commerce, the new CIT Law (i) specifies that foreign enterprises engaged in e-commerce and digital platform-based businesses will be deemed taxpayers, so long as they derive income from Vietnam, and (ii) broadens the concept of “permanent establishment” (PE) to include e-commerce and digital platforms through which foreign enterprises provide goods and services in Vietnam. However, where an applicable tax treaty provides for a different definition of a PE – which is likely, since traditional tax treaties often define a PE based on a physical presence test – the tax treaty will take precedence over domestic regulations.

Expanded list of tax-exempt incomes

The CIT Law introduces several new categories of tax-exempt income to promote the development of specific sectors, for instance:

a. R&D, innovation and digital transformation: (i) income generated from innovation and digital transformation activities (this income is tax-exempt for a period of up to three years); (ii) funds and sponsorships received from unaffiliated enterprises for scientific research, technology development, innovation and digital transformation;

b. Green economy and sustainability: (i) income from the interest on green bonds; (ii) income from the initial transfer of carbon credits and green bonds; and

c. Government support: direct support from the state budget and the Investment Support Fund established by the Government.

Revisions to deductible expenses

To be considered as deductible expenses, an enterprise’s expenses must be (i) actual expenses incurred in connection with its business activities or other actual expenses as prescribed by laws, and (ii) supported by adequate invoices and non-cash payment vouchers in accordance with the laws.

There is a key change pertaining to the non-cash payment threshold for expense deductibility. Whereas the current law sets this threshold at VND 20 million, the new CIT Law itself does not specify a monetary value. Instead, enterprises may refer to the Draft Decree, which is expected to regulate that non-cash payment is required for expenses of VND 5 million or more, aligning with the regulations on value added tax.

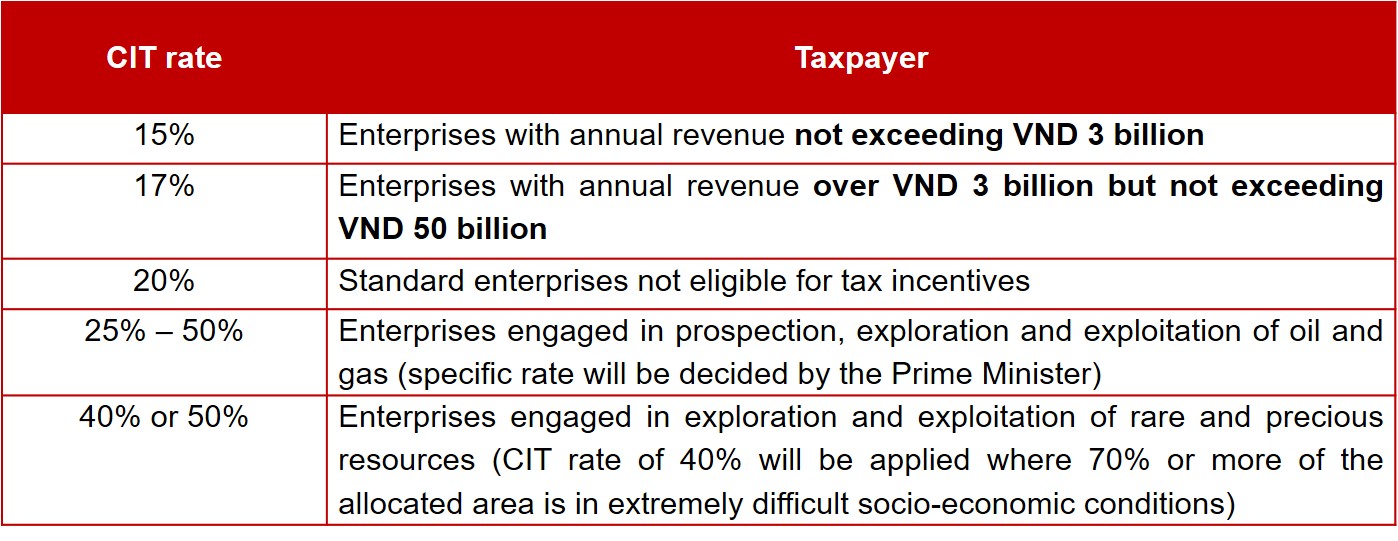

Revisions to CIT rates

While the standard CIT rate for most enterprises remains at 20%, consistent with the current law, two new, lower preferential rates (i.e., 15% and 17%) are introduced by the new CIT Law to support small and medium-sized enterprises (SMEs). For resource-based industries, the CIT Law maintains higher tax rates with slight adjustments.

Of note, the revenue used to determine an enterprise’s eligibility for the 15% and 17% tax rates is the total revenue from the immediately preceding tax period. However, these favourable tax rates shall not apply to exceptional incomes, including: (i) income from transfer of capital, capital contribution rights, real estate (except social housing projects), investment project (except mineral processing projects), project participation rights, rights to explore, exploit and process minerals, and offshore business activities; (ii) income from exploration and exploitation of oil, gas, minerals, and other rare and precious resources; (iii) income from production and trading of online games, or goods and services subject to special consumption tax (except projects for production and assembly of automobiles, airplanes, helicopters, gliders, yachts, and oil refining); (iv) income of a subsidiary or affiliated company where the related party is not eligible for the preferential tax rates; (v) other incomes not related to a company’s incentivised business activities (as per the Draft Decree); and (vi) other cases as specified by the MOF (as per the Draft Decree).

Revisions to CIT incentives

The CIT Law introduces a new provision (Article 12) to establish the principles for applying CIT incentives based on business sectors and geographical areas. This article also stipulates that the CIT Law’s provisions on CIT incentives shall prevail over other laws (except for the Capital Law and certain specific mechanisms stipulated in resolutions by the National Assembly), thereby ensuring uniform implementation of the laws and preventing overlapping or fragmented regulations.

A new CIT incentive structure for tax rates and tax holidays is introduced by the CIT Law, replacing the current law’s structure, specifically:

a. Incentive tax rates are classified into five categories based upon the eligible cases outlined in Article 12, as follows: (i) 10% tax rate for 15 years; (ii) 10% tax rate; (iii) 15% tax rate; (iv) 17% tax rate for 10 years; and (v) 17% tax rate.

b. Tax holidays are classified into two categories, as follows: (i) a tax holiday of 4-year exemption followed by a 9-year 50% reduction shall be offered for projects enjoying the 10% preferential tax rate in item (a-i) above, and projects involving socialised sectors such as education, vocational training, healthcare, culture, sports, and environment in areas with difficult or particularly difficult socio-economic conditions; and (ii) a tax holiday of 2-year exemption followed by a 4-year 50% reduction shall be offered for projects enjoying the 17% preferential tax rate in item (a-iv) above.

With regard to the scale increase, capacity enhancement, technology innovation, pollution reduction, or environmental improvement of an ongoing project (expansion investments) under Article 12 of the CIT Law, the additional income from expansion investments will benefit from the same tax incentives as the ongoing project, without the need for separate accounting. Of note, in cases where the ongoing project has already exhausted its tax incentive period, the additional income from the expansion investments will be considered for tax exemption and reduction in accordance with the laws, but not for any preferential tax rate.

The new CIT Law also introduces two new instances of tax exemptions, namely (i) newly established SMEs originating from household businesses (CIT-exempt for two consecutive years from the start of taxable income); and (ii) public scientific and technological organisations and public higher education institutions operating on a non-profit basis.

Proposed changes for capital transfers

In addition to detailed guidance for the CIT Law, another significant change proposed by the Draft Decree is the new provisions concerning CIT on capital transfers, which may have substantial impacts on M&A transactions, as follows:

Anti-Bribery and Corruption Policy: LNT & Partners has issued and maintained the policy in complying with all applicable laws and regulations on bribery and corruption in Vietnam and worldwide.